Starting or Running a U.S. LLC from the UK: What You Need to Know

Harrison Swift

June 20, 2026

We’re seeing a growing number of enquiries from individuals who either want to set up a U.S. LLC while living in the UK—or already have one and are planning to relocate here.

In both cases, the same issue arises: what looks simple on paper often becomes highly complex in practice.

The idea of a U.S. LLC is often marketed as flexible, tax-efficient, and easy to run. But when you introduce UK tax residency into the equation, the reality is very different.

Let’s unpack why.

1. The "Tax-Free" Myth Doesn't Apply to UK Residents

A common driver behind forming a U.S. LLC is the belief that it offers low or even zero tax. That might be true in very specific U.S.-based scenarios—but it doesn’t translate across borders.

If you’re a UK tax resident, the UK taxes you on your worldwide income and may impose additional reporting requirements. That means:

- Profits from a U.S. LLC are still potentially taxable in the UK.

- The UK may not treat the LLC the same way the U.S. does (more on that below).

- You could end up with complex reporting requirements in both countries.

In short, forming a U.S. entity doesn’t remove your UK tax obligations.

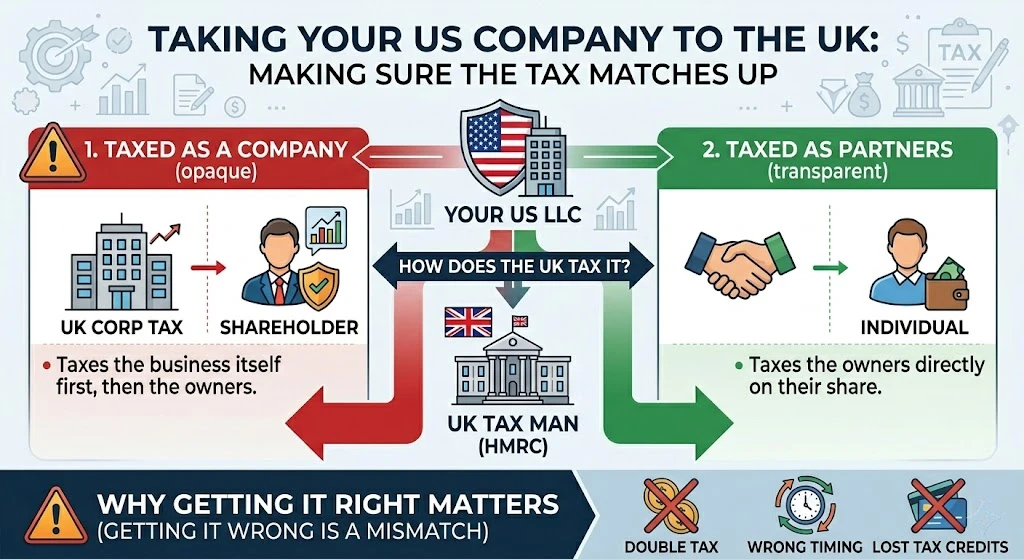

2. Mismatch in Entity Classification

Here’s where things get particularly tricky.

In the U.S., an LLC is often treated as a “pass-through” entity. However, HMRC doesn’t automatically follow that treatment and applies its own analysis when determining how foreign entities should be classified for UK tax purposes.

Depending on the legal characteristics of the LLC and the facts involved, the UK may view the LLC as:

- Opaque (broadly similar to a company), or

- Transparent (broadly similar to a partnership or disregarded entity).

If the LLC is treated as opaque for UK tax purposes, this mismatch can lead to:

- Double taxation in certain scenarios.

- Timing differences in when income is taxed.

- Limited or no access to foreign tax credits.

If the LLC is treated as transparent for UK tax purposes, this can also lead to:

- Timing differences in when income is recognised and when foreign tax credits become available.

Getting this wrong is one of the most common—and costly—pitfalls.

3. U.S. Compliance Is Not Optional

Even if you’re living entirely in the UK, a U.S. LLC brings U.S. filing obligations.

Depending on the circumstances, these may include:

- Annual federal partnership filings for multi-member LLCs.

- State-level filings and fees.

- Forms such as Form 5472 for certain foreign-owned U.S. LLCs, where penalties for non-compliance can be significant.

Many people assume that “no U.S. tax” means “no U.S. filing.”

Unfortunately, that’s not how it works.

4. Banking and Substance Challenges

Opening a U.S. bank account as a non-resident can be difficult, and many founders rely on fintech alternatives that may not fully meet business needs.

From a UK perspective, there is a more fundamental issue.

If you’re running the business from the UK, HMRC may argue that the central management and control is in the UK.

This can result in the LLC being treated as having a UK permanent establishment, UK taxable presence, or potentially UK tax residence.

5. The "Anson Argument" – Not a Shortcut

Some advisers and online forums point to Anson v HMRC as a basis for achieving favourable UK tax treatment of U.S. LLC income.

In practice, relying on Anson is far from straightforward.

HMRC has made it clear that it does not accept a blanket application of the decision. The case turned on very specific facts about the LLC’s legal structure and profit entitlement—facts which many modern LLCs do not replicate.

As a result:

- HMRC is likely to challenge positions based on Anson without strong technical grounding.

- The burden of proof sits with the taxpayer.

- Disputes can be lengthy, costly, and uncertain.

Any reliance on Anson should generally only be considered where:

- The facts closely align with the case.

- You have clear, written advice from a UK specialist adviser (typically tax counsel or a solicitor).

- The commercial benefit justifies the complexity and risk.

A Note on Practical Application

This is not to suggest that Anson-based positions are never appropriate.

We do act for clients where an Anson-based analysis is relied upon—but only after:

- Detailed review of the LLC’s legal characteristics.

- Collaboration with specialist UK legal advisers.

- A clear understanding of HMRC’s likely challenge position.

- A conclusion that the overall outcome justifies the risk and complexity.

These are not off-the-shelf solutions. They are highly fact-specific and require robust legal grounding, documentation, and ongoing oversight.

6. "Management Company" Structures – Not the Fix They Appear to Be

Another trend we are seeing is the suggestion that a UK limited company can provide services to a U.S. LLC under an arm’s length arrangement, with profits intentionally split between the two entities.

This is often presented as a workaround. In reality, it rarely resolves the underlying issues.

Risks include:

- Transfer pricing challenges.

- Profit diversion scrutiny.

- HMRC applying substance-over-form principles.

- Increased administrative complexity.

In many cases, this adds cost and risk without materially improving the tax outcome.

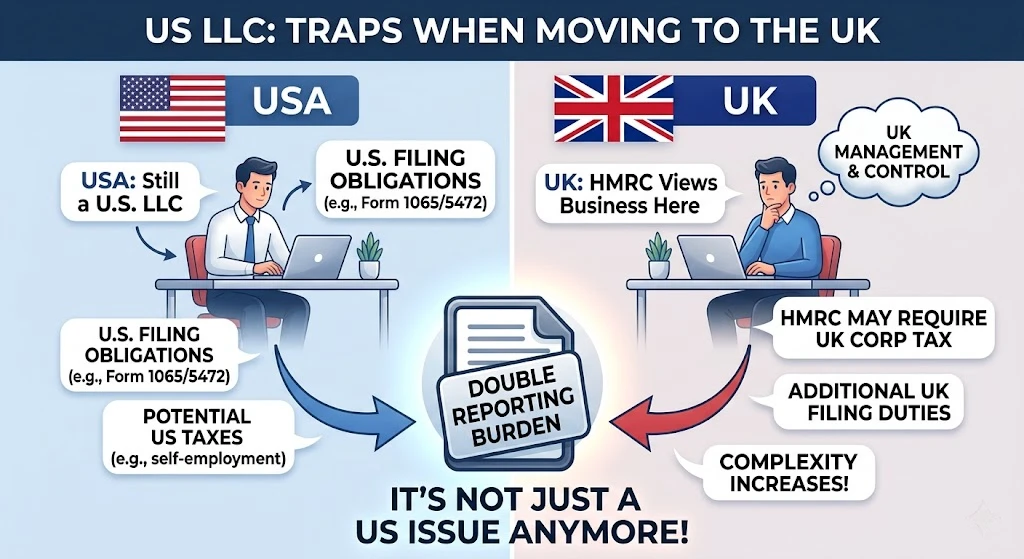

7. Moving to the UK with an Existing U.S. LLC? The Risks Don't Go Away

A common misconception is that once an LLC is established, it can simply be run from anywhere.

In reality, relocating to the UK with an existing U.S. LLC often creates the same—or greater—issues.

From a UK perspective, what matters is where the business is managed and controlled.

If that shifts to the UK:

- The LLC may have a UK taxable presence or UK tax residence.

- Profits may become subject to UK corporation tax.

- Additional UK filing obligations may arise.

- U.S. compliance obligations will still remain.

Why This Catches People Out

Many individuals assume:

“It’s a U.S. company, so it stays a U.S. tax issue.”

But HMRC looks at:

- Where decisions are made.

- Where the business is directed.

- Where value is created.

If that’s the UK, the UK will expect to tax it accordingly.

Practical Reality

We regularly see individuals who:

- Set up an LLC while living abroad.

- Later move to the UK.

- Continue operating as before.

…and only then discover that:

- They now have dual reporting obligations.

- The structure no longer achieves the intended outcome.

- Fixing it later is costly and complex.

8. The Rules Continue to Evolve

As of 2026, the UK government and HMRC continue to scrutinise the tax treatment of hybrid entities and cross-border structures, including U.S. LLCs and other entities that can create differences between U.S. and UK tax outcomes.

Following developments and announcements made during 2025 and 2026, further consultation and policy consideration in this area remain possible. While no comprehensive reform has yet been implemented, taxpayers should be aware that the treatment of certain cross-border structures may continue to evolve.

The direction of travel appears to be toward greater scrutiny of arrangements that create timing differences, mismatches in tax treatment, or opportunities for double non-taxation.

As a result, structures that appear effective today may not necessarily produce the same outcomes indefinitely. Anyone establishing or operating a U.S. LLC while resident in the UK should ensure their arrangements are reviewed periodically to reflect changes in legislation, HMRC practice, and case law.

9. Increased Complexity Without Clear Benefit

For many UK-based individuals, a U.S. LLC introduces:

- Additional compliance.

- Higher advisory costs.

- Cross-border tax complexity.

…without delivering meaningful advantages.

In many cases, simpler UK-based structures are more effective.

10. When These Structures Are Done Properly

It’s important to be clear—this is not an area we advise against categorically.

We act for a number of clients with U.S. LLC structures, including those:

- Operating internationally.

- Managing cross-border ownership.

- Navigating UK/U.S. tax differences.

In these cases, the structure works because:

- It has been designed with both jurisdictions in mind.

- The technical position is properly supported.

- The commercial rationale is clear.

- The client understands the compliance burden and cost profile.

Where those elements are missing, problems tend to follow.

Final Thoughts

The appeal of a U.S. LLC is understandable—but for UK residents, it is not a plug-and-play solution.

Done casually, it can lead to:

- Unexpected tax exposure.

- Structural inefficiencies.

- Ongoing compliance issues.

Done properly, with the right advice, it can form part of a coherent and effective international structure.

The difference is in the level of planning.

Whether you are:

- Considering setting one up, or

- Already operating one and moving to the UK, the key is the same:

Assess the position properly before issues arise—not after.

Disclaimer

This article is provided for general informational purposes only and does not constitute legal, tax, accounting, or other professional advice. The application of tax laws and regulations can vary significantly based on individual circumstances, and the information contained herein may not reflect the most current legal, regulatory, or judicial developments.

This article has been prepared by U.S. Enrolled Agents (EAs) and UK tax professionals at Harrison Swift. However, it is intended solely as general information and should not be relied upon as professional advice.

No reliance should be placed on this content without obtaining advice tailored to your specific circumstances from appropriately qualified legal and/or tax advisers. Neither the author nor the firm accepts any liability for any loss arising from reliance on the information contained in this article.

Readers should seek tailored advice before undertaking any action based on the matters discussed.

Complex Cross-Border Tax Rules? We’re Here to Help

Have Any Question?

Consult Our Expert Tax Consultants for your Cross-Border Taxes!

- +44 (0)2034354425

- info@harrisonswift.com

Categories

Our Blog

Latest Blog & Articles

Starting or Running a U.S. LLC from the UK: What You Need to Know

Starting or Running a U.S. LLC from the UK: What You Need to Know Harrison Swift June 20, 2026...

I Thought My Green Card Expired. The IRS Didn’t.

I Thought My Green Card Expired. The IRS Didn’t. Harrison Swift June 12, 2026 Tax The Forgotten Tax Rules...

IRS Payments Are Going Digital: What Overseas Taxpayers Need to Know

IRS Payments Are Going Digital: What Overseas Taxpayers Need to Know Harrison Swift May 25, 2026 Tax The IRS...