Inheriting a U.S. IRA? What UK Taxpayers Need to Know (2026 Update)

Harrison Swift

May 14, 2026

If you live in the UK and have inherited money from a relative in the United States, you may have come across something called an IRA — an Individual Retirement Account. These are common U.S. pension-style accounts, and if you’ve received a distribution from one, you may be wondering:

Will I have to pay UK tax on it?

The answer is: very likely yes — even if tax has already been paid in the U.S. And even if it was a one-off, inherited lump sum.

In this post, we explain how inherited IRA distributions are taxed in the UK, and how HMRC now applies the UK–US tax treaty to these payments — including important updates every beneficiary should know in 2026.

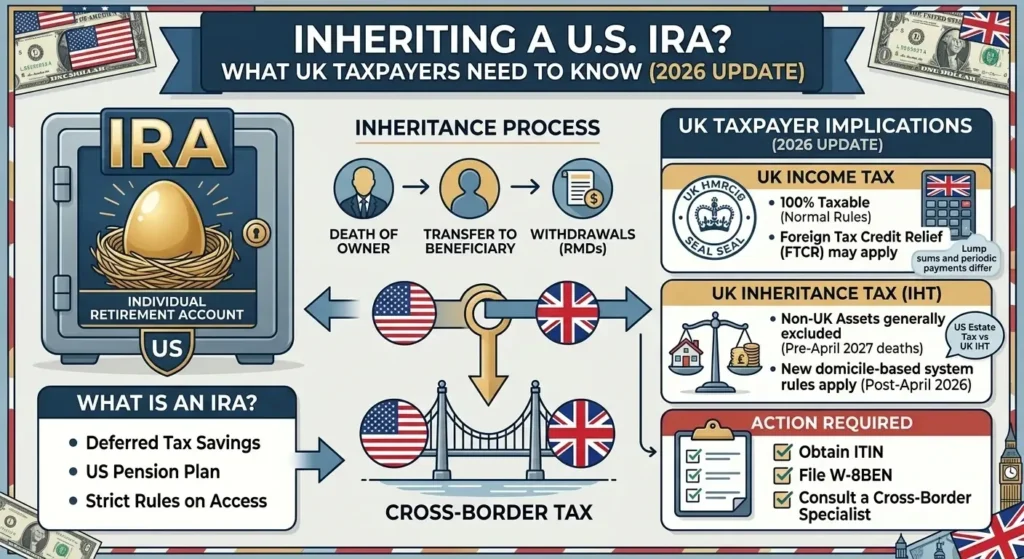

What Is an IRA?

A U.S. IRA (Individual Retirement Account) is a personal retirement savings vehicle. There are different types — the most common are Traditional IRAs and Roth IRAs — and both may form part of someone’s estate after they pass away.

As a UK resident, if you inherit an IRA, the U.S. institution may allow you to take:

- One-off (lump sum) distributions

- Periodic payments over time

In either case, the payment you receive is known as a distribution — and it’s important to understand how that is taxed in the UK.

Are Inherited IRA Distributions Taxed in the UK?

Yes — unless they fall under a specific exemption or relief, IRA distributions are taxable in the UK as foreign income.

Whether you receive the entire account in one go, or in monthly payments, HMRC expects you to report the distribution on your Self Assessment tax return.

In the past, there was some belief that lump sum payments might be fully exempt from UK tax under the UK–US tax treaty. However, this is no longer the case.

What Changed? HMRC’s New Position on “Lump Sums”

In 2025, HMRC clarified its position on lump sum pension distributions from the U.S., including IRAs.

Although the UK–US tax treaty (Article 17) gives the U.S. exclusive taxing rights over lump sum payments, HMRC now applies the treaty’s “savings clause” (Article 1(4)), which overrides this exemption.

In plain terms:

HMRC does tax lump sum IRA payments received by UK residents — even if the treaty appears to give taxing rights to the U.S. alone.

That means one-off, inherited distributions from a U.S. IRA are taxable in the UK. This includes distributions that are:

- Irregular or one-time

- Not part of a structured payout plan

- Received from a deceased relative’s IRA

What About the U.S. Tax That’s Already Been Paid?

In most cases, the U.S. institution handling the IRA will withhold 30% tax on the distribution if you’re a UK resident (classified as a “non-resident alien” under U.S. tax rules).

The good news is: if the payment is treated as a lump sum, you can usually claim the U.S. tax paid as a credit against your UK liability using Foreign Tax Credit Relief through your Self Assessment tax return.

This helps reduce the risk of double taxation — although the income must still be reported in the UK, even where the foreign tax credit fully offsets any UK tax due.

The treatment is different for periodic pension payments. Under the UK–US tax treaty, periodic IRA or pension distributions are generally taxable only in the UK. In these cases, U.S. withholding tax may not qualify for Foreign Tax Credit Relief in the UK, meaning taxpayers may instead need to reclaim the U.S. tax directly from the IRS.

Because the interaction between the treaty, HMRC guidance, and IRS withholding procedures can be complex, professional advice is strongly recommended before filing.

What If You Have No Other Income?

If the IRA distribution is your only income, and the total amount received is below the UK personal allowance (currently £12,570), then no UK tax may be payable — but you’ll still need to:

- Report the distribution

- Claim foreign tax credit relief if U.S. tax was withheld

Failing to do so could result in penalties or loss of credit for U.S. tax already paid.

What Should You Do?

Here’s what we recommend if you’ve received (or expect to receive) an inherited U.S. IRA distribution while living in the UK:

Gather Documentation

You should keep:

- Statements of distribution from the IRA provider

- Confirmation of any U.S. tax withheld (Form 1042-S or similar)

- Executor letters or probate documents (if applicable)

Determine the Nature of the Distribution

Is it:

- A one-off lump sum?

- A periodic payment?

This distinction affects how treaty relief and foreign tax credits apply.

Report the Income Properly

Your Self Assessment return should include:

- The gross amount of the distribution

- Details of any U.S. tax withheld

- Any claim for foreign tax credit relief

- An explanation of the nature of the payment if required

Seek Advice If:

- You receive multiple distributions

- The U.S. tax withheld was unusually high or low

- The IRA contains complex or non-cash assets

- You are unsure how the treaty applies to your situation

Real-Life Example

You inherit $11,000 from your father’s U.S. IRA and receive it as a one-time payment. The U.S. custodian withholds 30% tax — $3,300 — and you receive $7,700 in your account.

In the UK:

- You must report the full $11,000 as foreign income

- You may be entitled to claim the $3,300 U.S. tax as a foreign tax credit against any UK tax due

- If this is your only income and you’re under the personal allowance, no UK tax may ultimately be payable — but the income must still be declared to HMRC

Final Thoughts

The rules around inherited U.S. IRAs have evolved — and the days of assuming “lump sums aren’t taxed in the UK” are over.

HMRC’s updated guidance means that even one-off inherited IRA lump sums may now fall within the scope of UK taxation, although relief may be available for U.S. tax already paid.

The good news is that proper reporting and treaty relief can often prevent double taxation — but only if the distributions are handled correctly.

At Harrison Swift, we specialise in helping individuals navigate complex cross-border tax issues, including inherited U.S. retirement accounts and foreign income reporting.

If you’ve received an IRA distribution — or expect to — we can help you:

- Understand your UK tax position

- Complete your tax return correctly

- Claim available treaty reliefs and foreign tax credits

- Avoid unnecessary tax or compliance issues

Get in touch today to speak to one of our advisers.

Legal Disclaimer

The information in this article is provided for general informational purposes only and does not constitute legal, tax, or financial advice. While every effort has been made to ensure the accuracy of this content at the time of writing, tax laws, treaty interpretations, and HMRC guidance are subject to change.

You should not rely on this article as a substitute for personalised advice from a qualified tax professional. Tax treatment will depend on your individual circumstances.

Harrison Swift accepts no responsibility for any loss or damage arising from reliance on the information contained in this article. For advice tailored to your circumstances, please contact us directly.

Complex Cross-Border Tax Rules? We’re Here to Help

Have Any Question?

Consult Our Expert Tax Consultants for your Cross-Border Taxes!

- +44 (0)2034354425

- info@harrisonswift.com

Categories

Our Blog

Latest Blog & Articles

Inheriting a U.S. IRA? What UK Taxpayers Need to Know (2026 Update)

Inheriting a U.S. IRA? What UK Taxpayers Need to Know (2026 Update) Harrison Swift May 14, 2026 Tax If...

When Does My US Citizen Child Need to File with IRS?

When Does My US Citizen Child Need to Start Filing with the IRS? Harrison Swift September 18, 2025 Tax...

Navigating RSUs Across the US and UK: What You Need to Know

Navigating RSUs Across the US and UK: What You Need to Know Harrison Swift September 18, 2025 Tax Restricted...